It has been some time since we covered AvalonBay Communities, Inc. (NYSE:AVB). On our last take, we preferred to stay out of this REIT as the high multiples were just too rich for our blood. We also expected REIT investors to face a harsher climate from higher interest rates. Specifically we wrote.

AVB is a solid long-term play on the residential market. Current valuation metrics are on the higher side, but whether you get it cheaper will depend on where the 10-year Treasury rate goes. We think significantly higher rates are in the offing in the next 12 months and in general are not chasing high-multiple REITs. We rate this currently at neutral but do recognize the quality of this company. For our residential investments, we are going for the Boardwalk Empire.

Source: A Quality Residential REIT

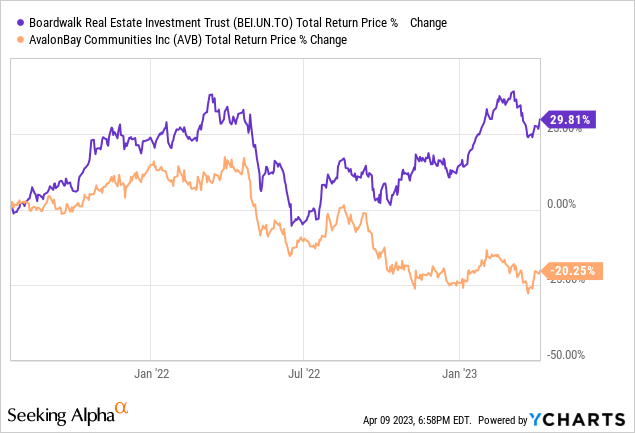

The Boardwalk Empire was a reference to Boardwalk Real Estate Investment Trust (OTCPK:BOWFF), one of the rare residential REITs that was cheap at the time. AVB tried hard to keep up with the Alberta Stallion, but lagged by over 50% in the last 20 months.

Data by YCharts

We look at where AVB stands today to see if we can make a reverse call. As we do that, keep in mind that we recently rated Boardwalk as a sell.

Recent Results

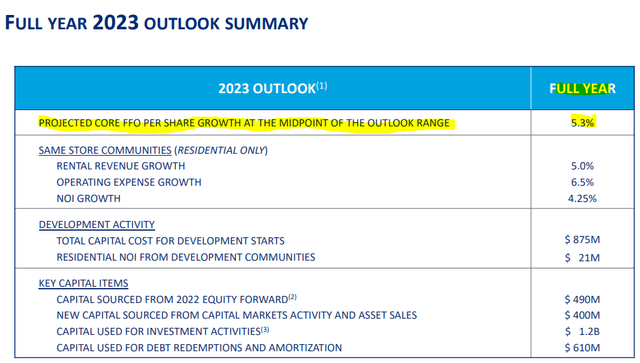

Both Q3-2022 and Q4-2022 missed slightly on the funds from operations (FFO) numbers. AVB walked down analysts slightly for both Q1-2023 and the full year.

AVB Presentation

You can see that in the recent estimates.

Seeking Alpha

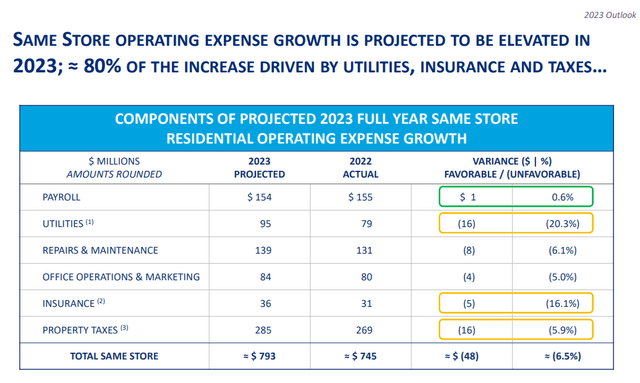

The culprits are from the expense side as insurance and utility costs are projected to rise sharply in 2023.

AVB Presentation

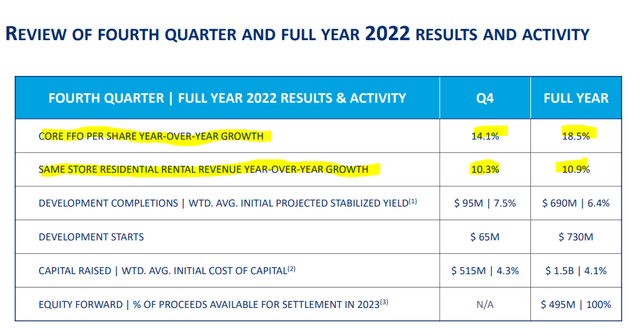

While there was a small mismatch in expectations, the core numbers for AVB continue to be incredibly strong.

AVB Presentation

Occupancy trended higher in the first two months of the year and like-term effective rent changes also accelerated ahead.

AVB Presentation

Outlook

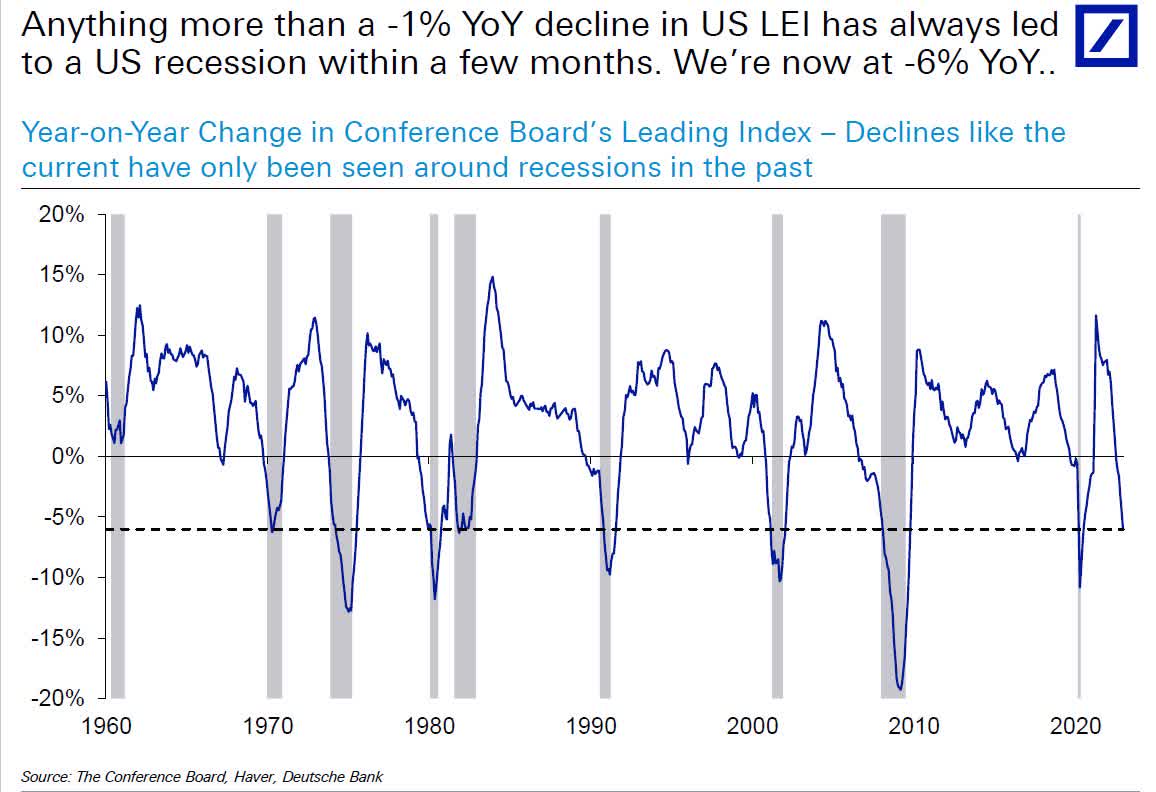

On the macro side there are three major forces intersecting to impact AVB. The first being what we see as a guaranteed recession at some point in 2023.

Deutsche Bank

The exact timing of this is irrelevant but the ultimate impact is anything but. The ability to pass on these rent hikes will be challenged in a downswing. Yeah, this may some counterintuitive to people saying “you have to live somewhere”, but that is our stand. That stand is bolstered by the second major force, supply. There is a lot of that coming on and we really mean a lot.

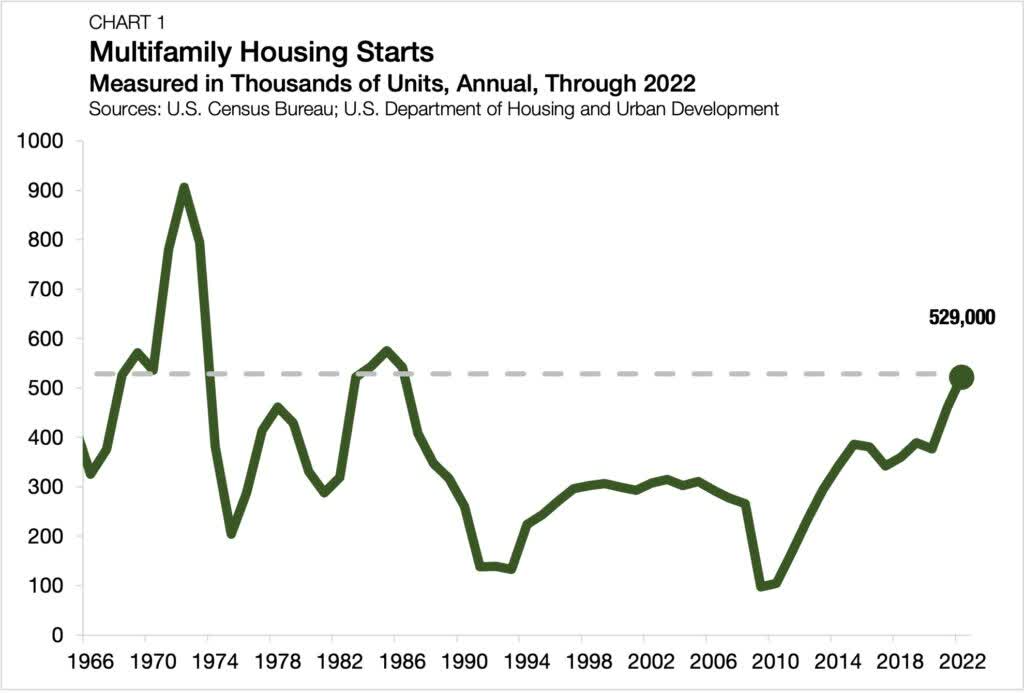

The multifamily construction sector has had more than its fair share of headwinds to navigate through in recent years. Supply chain disruptions, rising interest rates, and a structural shortage of skilled construction labor have made it more challenging to add supply quickly enough to meet demand. Nevertheless, despite the obstacles, 2022 was a banner year for multifamily construction starts. Last year, construction began on 529,000 new multifamily units — the highest on record since 542,000 units were started in 1986, according to the U.S. Census Bureau and the U.S. Department of Housing and Urban Development.

US Census Bureau

After reaching a low point of 97,600 annual multifamily construction starts at the close of the Great Recession in 2009, building activity has consistently risen, increasing in 10 out of 13 years.

This is coming from the dual forces of easy monetary policy and capital allocation errors. We always build for the last boom and this is no different. Apartments were hot and they were resilient during the last decade. Now we are building them in pretty massive amounts. All that supply should hit in 2024-2025.

Source: Arbor

The final point influences demand. The housing market is in a deep freeze and unlikely to thaw in 2023. Buying a new home is now prohibitively expensive for most that thought otherwise in 2021. This acts as a partial offset to both points above, but ultimately we don’t think it will be adequate to counteract them completely.

Valuation & Verdict

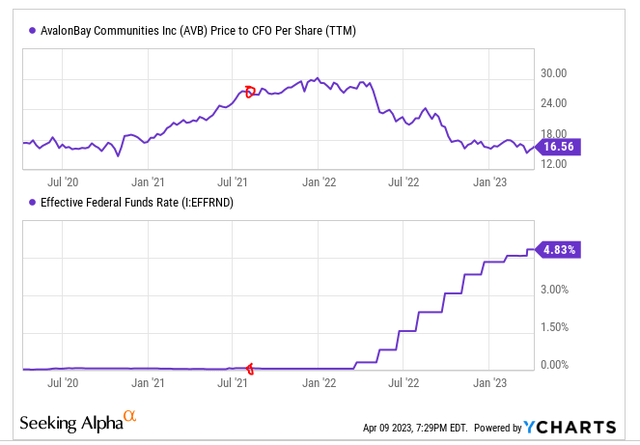

One of the most satisfying things in investing to see a thesis play out exactly as it was envisioned. Interest rates rose and valuation compressed. We have circled when we wrote our last piece.

Y-Charts

At the current numbers, AVB is certainly cheap relative to the last decade. But it is in no way, shape or form, cheap relative to where interest rates are. While the current NAV is higher than the stock price, we expect that to drift down as well as cap rates to blow out over time. So for the AVB investment case to work out, you need low interest rates or some more valuation compression. That said, when things get close to cheap enough, you can always play it using options. We did just that in November 2022.

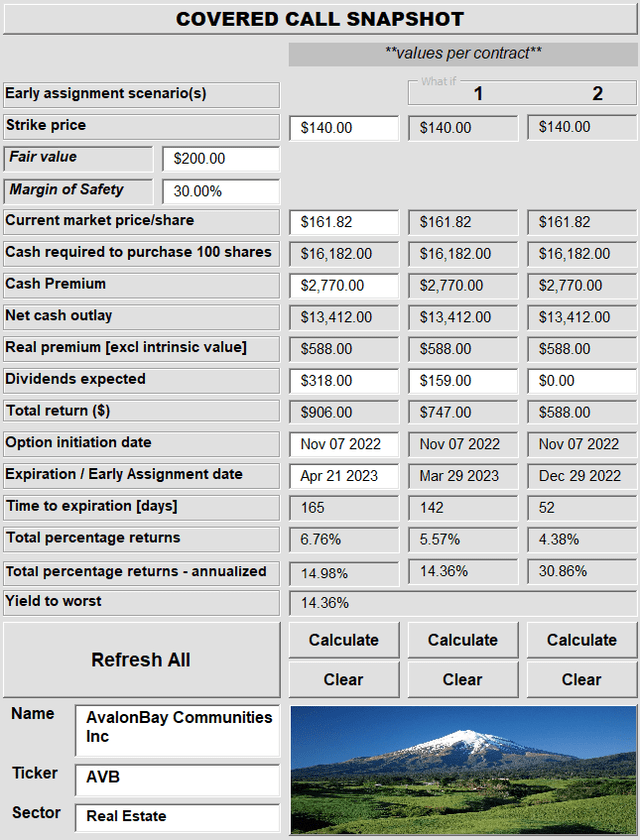

AVB has an estimated NAV today of close to $230/share and its balance sheet is in one of the best shapes it has ever been. Current credit ratings are at A3 for Moody’s and A- for S&P. We sold one covered call contract for AVB, $140 April 2023 with a $6.00 net premium.

Please use Buy-Write functionality and limit orders if this is a trade for you. Corresponding CSP is shown for those interested and can probably be done for around $5.40. Nearby strikes ($145 and $135) are also liquid and can be considered.

Interactive Brokers Nov 7, 2022

Covered Call $140 April 2023

Trade 315 CIP

Source: Trade 315 Conservative Income Portfolio [CIP]

So that trade explains where we stand and we will take a low risk 15% annualized yield any day. We are a buyer at $140.00 and while those shares will be called away in two weeks, we might land up writing more income plays near prices we see fit. We continue to rate AVB a hold here.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

")

")

")

")

: Positioned To Unlock Value Following Significant Investments")

")

")