")

")

Cipher Mining Inc. (NASDAQ:CIFR) is a company that specializes in developing and operating Bitcoin mining data centers. CIFR’s operations are based in Texas, fueled by low-cost fixed-price power. As the cryptocurrency market is bracing for the halving’s shake-up, CIFR’s strategy is to acquire assets at cyclical lows, maximize the use of power using efficient mining equipment and cost-effective power sources, optimize trading with participation in the energy market, and improve production pre-halving. My valuation:

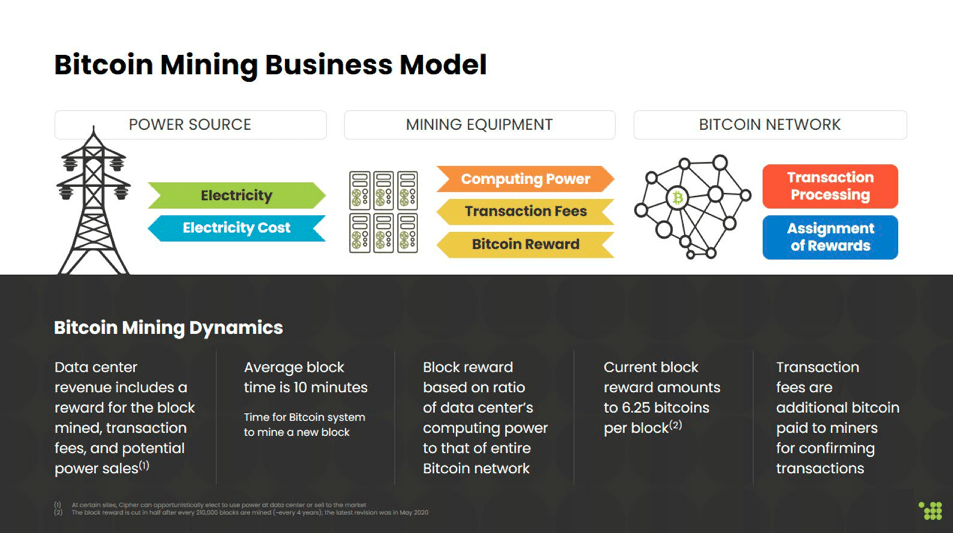

A Mining Operation: Business Overview

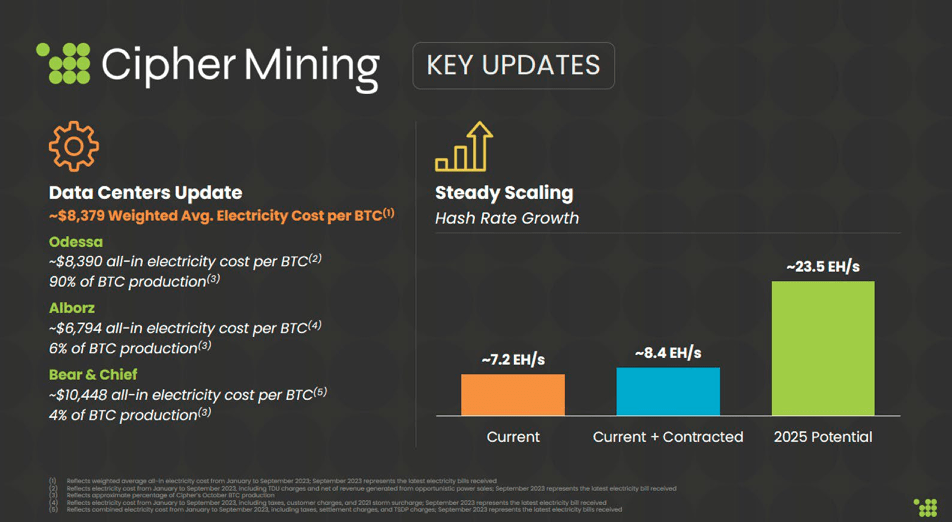

Cipher Mining is a company that runs Bitcoin mining data centers in three locations in Texas: Odessa, Alborz, and Bear and Chief facilities located near Andrews. These data centers have operation capacity of 207 MW, 40 MW, and 20 MW, respectively. The number of mining bitcoins YTD through October 2023 is 3,531 in Odessa with an average electricity cost per Bitcoin of $8,390, 603 in Alborz with an electricity cost per Bitcoin of $6,794, and 421 in Bear and Chief facilities with an electricity cost per Bitcoin of $10,448. Approximately 96% of the CIFR’s facilities use low-cost, fixed-price power. The CIFR operational efficiency is based on the low cost in the industry at roughly $0.027 per kilowatt hour. Naturally, electricity costs aren’t the only variables pertinent from a business perspective, but evidently, CIFR has access to cheap electricity, which sets it up for profits at higher Bitcoin prices.

In November 2023, CIFR completed the Odessa data center, leading to a hash rate capacity of 7.2 exahash per second [EH/s]. Moreover, the company signed an agreement to buy a new site in Texas with the approval of the Electric Reliability Council of Texas [ERCOT]. ERCOT schedules power distribution and manages the energy market in Texas. The new facility, Black Pearl, is expected to be functioning by 2025 with 300 MW of energy. The monthly sale of Bitcoin covers CIFR’s operating expenses and CapEx. They aim to build their bitcoin inventory with the surplus while investing in growing its infrastructure. Additionally, CIFR can sell back electricity to the grid on the Odessa site, and they report it as a Bitcoin equivalent.

CIFR invested in 1.2 EH/s of S21 rigs to be delivered in the first half of 2024. The Odessa facility achieved a high site hash rate of 6.24 EH/s. The company plans to expand its operations and increase its capacity to 23.5 EH/s by the end of 2025. CIFR’s acquisition of computational power at a competitive price will improve its efficiency and Bitcoin mining output, which is essential, especially near the halving that will reduce the block reward from 6.25 to 3.125 Bitcoins.

Source: Cipher Mining Business Update Presentation, November 2023.

The next halving will be in April 2024, and it will affect a company like CIFR due to the reduced revenue per block and the intensification of competition because each miner will try to be more efficient. In the last halving, the Bitcoin price rose to a maximum of a year or a year and a half after. This price increase counteracts the negative effect of the diminishing block reward. However, the CIFR position will depend on its efficiency and market condition. On the other hand, the impact of the next halving remains to be seen and may differ from previous ones because the current economic circumstances are different from those in the last halving.

Halvings are huge events in crypto, and their consequences are highly unpredictable. The generally accepted view is that halvings reduce the Bitcoin mining rewards by half, reducing the selling pressure on Bitcoin. As a result, the price rises after halvings due to the lower supply, which has been the case historically. However, from a mining perspective, there’s a lag between the price increase and the immediate rewards being cut in half. This period creates uncertainty for miners as they have to perform the same amount of work for half the pay, and relying on prices doubling to make up for the reduced rewards is inherently speculative. Moreover, Bitcoin’s hashing rate has consistently trended higher over time, meaning miners must keep up with their processing power or see significant losses.

CIFR’s Solid Cash Flow and Crypto Shifts

In the Q3 2023 Earnings Call, the CIFR executives were pleased with the performance during the first full summer operating in Texas despite the challenging environment with record heat and power reduction by the provider they achieved to optimize the performance. Heat is a big factor for mining companies as computers and processors wear down quickly due to heat. Generally speaking, the warmer the environment, the faster the equipment will wear down. This is why mining companies tend to prefer colder locations because the heat generated from mining is offset by the room temperature, prolonging the useful life of the mining equipment. So it’s promising to see that despite the recent hot weather, CIFR managed to perform satisfactorily.

Moreover, Q3 2023 was solid related to cash flow and liquidity. The Odessa site was fully running and generated $30.3 million for the three months ending September 30, 2023. The cost of revenue was $13 million due to power costs. Additionally, they reported sales of power at $2.7 million.

Source: Cipher Mining Business Update Presentation, November 2023.

Furthermore, from August to October 2023, some events had an incidence in the Bitcoin market, its price, and its hash rate. On August 29, Grayscale won an SEC lawsuit for its Bitcoin [ETF] review. Grayscale aims to convert its Grayscale Bitcoin Trust [GBTC] into a listed Bitcoin exchange-traded fund ETF. Theoretically, if GBTC converts into an ETF, it’d unlock its Bitcoin at market prices. This is potentially a big event as GBTC holders would quickly realize the discount to NAV, which currently stands at around 13.71%. This means that this particular discount to NAV is also an indicator of the likelihood of the ETF conversion being approved. The lower the discount, the higher the possibility, as the market judges. It’s generally accepted that a Bitcoin ETF would create a seamless investment vehicle for investors in traditional markets, bringing additional demand for Bitcoin and supporting higher prices.

Accordingly, on September 28, the deadline for Bitcoin ETF approval was delayed to early 2024. On September 22, the Financial Accounting Standards Board [FASB] ruled on digital assets with guidelines for companies to account for cryptocurrencies on their financial reports. These guidelines can build confidence in investors, bringing transparency to how these assets are measured in financial statements. This ruling also gives regulatory legitimacy to crypto assets. Finally, the hash rate grew due to the increment of computational power with the development of new technologies. These positive developments paint a potential turning point for the crypto markets after a dismal crash in 2022.

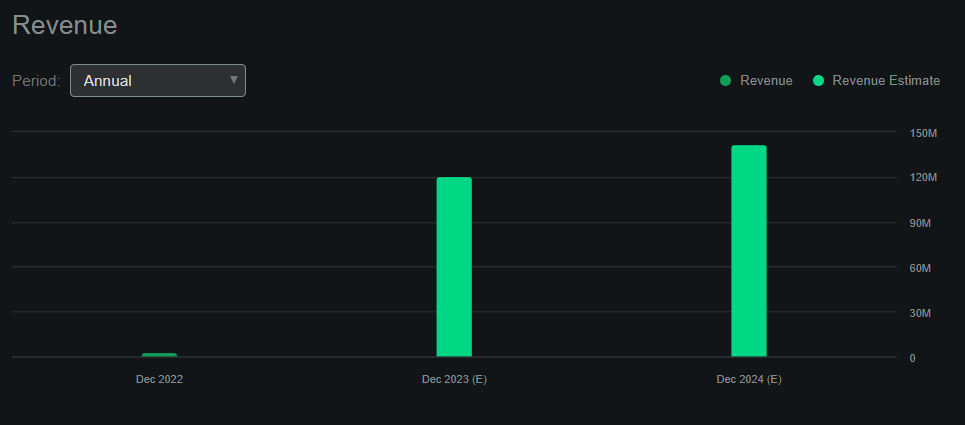

Analysts expect CIFR to generate roughly $141.7 million in revenues in 2024. (Seeking Alpha.)

Still Expensive: Valuation Analysis

From a valuation perspective, one of the most telling slides from CIFR’s investor presentation was their Bitcoin-mined target. They claim that pre-halving, they can mine 14.9 Bitcoins per day. We can infer that post-halving, they’ll likely mine half of that, or 7.45 Bitcoin daily. We don’t know what will be the Bitcoin price by then, but if we assume that Bitcoin rises to $50,000 in the long run after this halving as it has done in previous halvings, then that’d imply a daily revenue run rate of $372,500, or roughly $136.0 million.

CIFR trades at a $629.8 million market cap, implying a 4.63 P/S ratio. This is relatively expensive as the sector’s median P/S ratio is about 2.82, or roughly half of CIFR’s multiple. Naturally, if Bitcoin rises much above $50,000, this valuation multiple would improve proportionally, though that ventures into highly speculative territory. In my view, CIFR trades at a high multiple, and given that there are other alternatives in the sector at better valuation multiples, I think that makes CIFR a “hold” for now.

Despite CIFR’s recent pullback, it trades at a relatively high multiple. (TradingView.)

Conclusion

Overall, CIFR is a relatively simple business with its Bitcoin mining operation. There’s nothing particularly special about the firm other than its high-potential EH/s. In the long run, bitcoin mining companies should do well if Bitcoin continues to increase in price. However, if the price remains relatively stable or stagnates over many years, the hashing rate required to mine Bitcoin and the Bitcoin reward itself will pressure CIFR’s business over time. Thus, this is why I believe it’s vital to invest in miners only at highly favorable valuation multiples, and currently, CIFR seems rather expensive. Therefore, I believe CIFR is a “hold” for now.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here

")

Q3 2024 Earnings Call Transcript")

")