")

Over the past year I have found a number of interesting players in the banking sector. Some of these have been enterprises that I became very bullish on that went on to achieve some rather meaningful upside. Other opportunities have fallen short of expectations. Others, still, were firms that I did not have high hopes for and that went on to achieve the mediocre results I anticipated. In this final category one firm that I could point to as an example is Independent Bank Group (NASDAQ:IBTX).

With a market capitalization as of this writing of $1.87 billion, Independent Bank Group is not a particularly large regional bank. But it’s not exactly small either. Back in August of 2023, I decided to take a crack at the business, finding it an interesting opportunity since shares had not yet fully recovered from the crash that they experienced during the banking crisis that began in March. What I found, however, was that the stock probably did not deserve to trade much higher than where it was. The good news for shareholders was that, after experiencing some weakness when it came to things like deposits, fundamental improvements started to develop. But in spite of that, shares looked rather pricey and significant weakness on the bottom line caused me to take a more cautious approach to the business.

As a result, I ended up rating the bank a ‘hold’ to reflect my view that the stock would be unlikely to outperform the broader market for the foreseeable future. Since then, I ended up being mostly right. While the S&P 500 is up a robust 12.7% since the time that article was published, shares of Independent Bank Group have seen upside of a little more than half that at 6.7%. In some cases, one could argue that additional patience is required. But when you look at other factors such as the overall health of the business, it’s difficult to see what additional patience will buy you besides continued mediocre returns.

There remain better opportunities out there

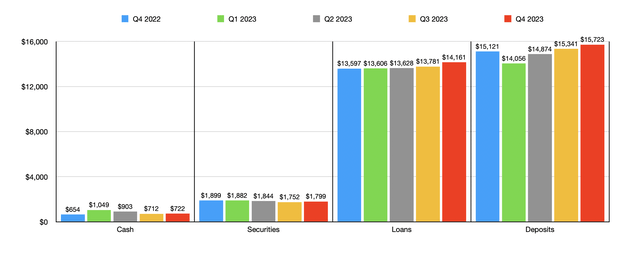

Back when I wrote about Independent Bank Group in August of 2023, we had data covering through the second quarter of that fiscal year. Today, that data now extends through the final quarter of 2023. To start with, we should touch on some of the good news. And that involves the deposits at the institution. You see, at the end of the 2022 fiscal year, Independent Bank Group boasted $15.12 billion worth of deposits. But in the first quarter of 2023, deposits plunged to $14.06 billion. Considering the banking crisis that had occurred and the high interest rate environment that we have had to deal with, this is not a terribly surprising scenario to see unfold.

Author – SEC EDGAR Data

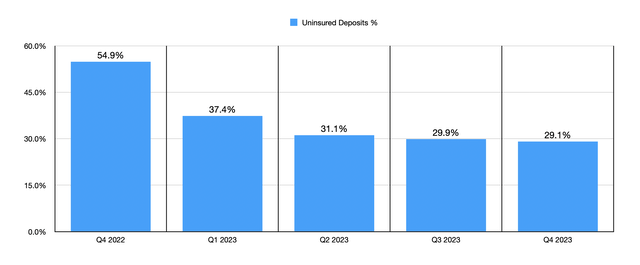

The good news for shareholders is that the bank began recovering almost instantly. By the end of the 2024 fiscal year, deposits had reached a new multi-year high of $15.72 billion. That’s an increase of $601.6 million compared to what the company ended 2022 at. It’s also important to note that about 29.1% of the firm’s deposits were uninsured. This is just below the 30% maximum threshold that I tend to prefer. This is a significant improvement over the 54.9% that were uninsured at the end of 2022 and the 37.4% that was seen at the end of the first quarter of last year. In fact, in each quarter from the final quarter of 2024 through the present day, an insured deposit exposure has declined.

Author – SEC EDGAR Data

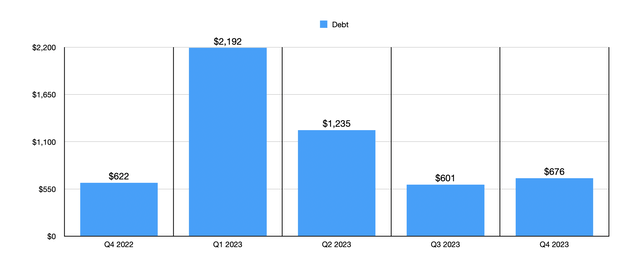

There is some other good news as well. The value of loans, for instance, continues to go up as well. Unlike deposits, there was not a quarter in which we saw a drop. From the end of 2022 through the end of 2023, loan values went from $13.60 billion to $14.16 billion. Cash on hand also increased nicely, climbing from $654.3 million to $722 million. The only decline that we saw during this time involved securities. These dropped modestly from $1.90 billion to $1.80 billion. Obviously, we should also talk briefly about debt. After spiking from $621.5 million at the end of 2022 to $2.19 billion in the first quarter of last year, debt has been falling. It did bottom out at $601.3 million in the third quarter before worsening slightly to $676.4 million at the end of 2023.

Author – SEC EDGAR Data

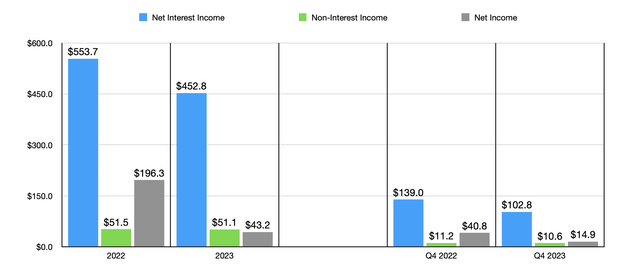

All of these are positives for the most part. The big negative, however, it’s that revenue and profits have dropped. In the chart below, for instance, you can see net interest income for the final quarter of the 2023 fiscal year. It totaled $102.8 million, which was well below the $139 million reported one year earlier. A rather large drop in the net interest margin for the bank from 3.49% to 2.49% was responsible for this. The fact that deposits outgrew the sum of loans, securities, and cash, also was a problem. Although deposits are desirable to have, when interest rates go up, the amount that management must pay in order to retain those deposits goes up as well. Non-interest income dropped slightly from $11.2 million to $10.6 million. That, combined with the aforementioned drop in net interest income, pushed net profits down from $40.8 million to $14.9 million.

Author – SEC EDGAR Data

In that same chart, you can see results for 2023 relative to 2022. As a whole, the picture looked very similar to what we saw for the final quarter on its own. There is one thing that, in my opinion, we need to bring up here. And then involves a couple of entries on the firm’s income statement for 2023 in its entirety. During that year, the company booked a $5.2 million impairment on some real estate. Furthermore, it incurred a $102.5 million charge under litigation expenses. Using the effective tax rate for 2023, I then calculated adjusted earnings for that year. Those came out to $132.1 million compared to the $196.3 million reported one year earlier and the official earnings for 2023 of $43.2 million.

Author – SEC EDGAR Data

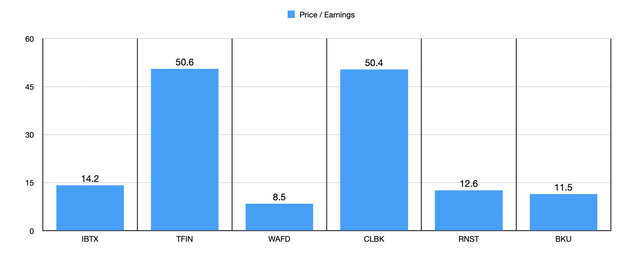

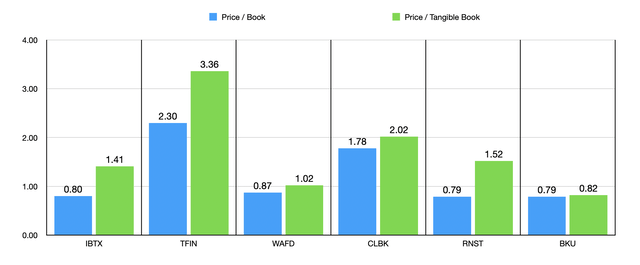

Using these results, I was then able to value the company on a price to earnings basis and compare it to five similar firms as shown in the chart above. Even using the adjusted earnings, the price to earnings multiple of 14.2 is quite high. Three of the five companies I compared it to ended up being cheaper than it. I then, in the chart below, performed the same type of analysis using both the price to book multiple and the price to tangible book multiple. When it comes to the price to book multiple, two of the five firms were lower than it, while when it came to the price to tangible book approach, the same holds true.

Author – SEC EDGAR Data

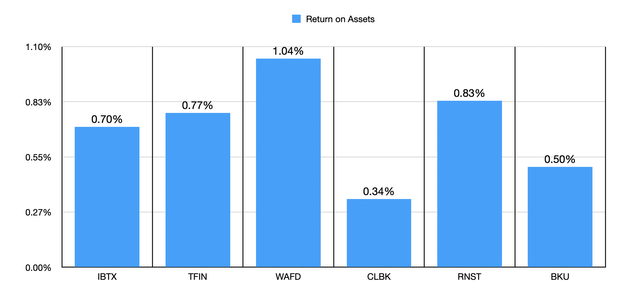

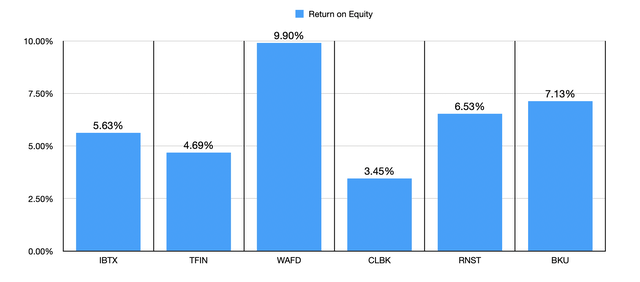

What we have here is an institution that, even in spite of some difficulties on the bottom line, is showing signs of improvement. However, while shares might not be outrageously priced compared to similar firms, both the price to earnings multiple and the price to tangible book multiple are higher than I would like them to be. Of course, if the quality of the earnings justifies this, then so be it. But I don’t believe that’s necessarily the case. In the first chart below, for instance, you can see the return on assets for Independent Bank Group. Two of the five companies ended up being lower than it, while three of the five came in higher. I then did the same thing in the subsequent table below involving the return on equity. In this case, two of the five firms were, once again, worse than our candidate.

Author – SEC EDGAR Data Author – SEC EDGAR Data

Takeaway

Based on the data in front of me, Independent Bank Group is not a great candidate. But it’s not a horrible one either. The firm is about the middle of the pack when it comes to most things and it is showing improvements where it counts. As a value investor who seeks market beating returns, however, this makes the firm a mediocre opportunity. So because of that, I’ve decided to keep the business rated a ‘hold’ for now.

Read the full article here

(NYSE:SNOW)")

")

Q4 2024 Earnings Call Transcript")