Q3 2024 Earnings Call Transcript")

")

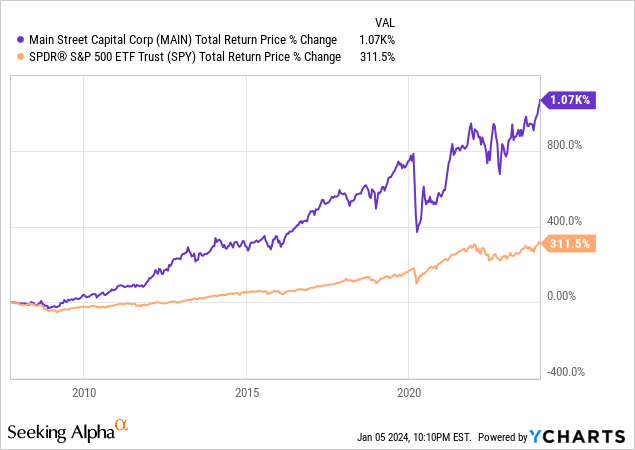

Main Street Capital (MAIN) and CION Investment Corporation (CION) are both high-yielding Business Development Companies (BIZD). MAIN, with its impressive track record of crushing both the broader BDC sector as well as the S&P 500 (SPY) over the long term, is a leading blue-chip BDC:

Meanwhile, CION, a relatively newer entrant to the publicly traded BDC space, has been making strides with its strategic investments and strong dividend yield. Moreover, with its steep discount to NAV and well-covered double-digit dividend yield, it appears as if it might offer compelling upside potential to investors at current prices.

In this article, we will compare these two BDCs side-by-side and offer our take on which is a Strong Buy right now.

MAIN Stock Vs. CION Stock: Quarterly Results

MAIN reported impressive Q3 results, including a significant increase in its net asset value per share by $0.64 (2.3% sequentially), primarily attributed to unrealized gains and retained earnings. Its core earnings per share saw a sequential growth of 3.8% and a notable 15.4% year-over-year increase. Last, but not least, the weighted average effective yield of MAIN’s portfolio was quite high at 12.8%.

CION’s third-quarter results were also quite strong, with net investment income of $0.55 per share and earnings per share reaching $0.87, providing significant coverage for the dividend and helping to boost NAV per share, which increased by $0.49 (3.2%) compared to the previous quarter. Moreover, management continued to buy back stock at a steep discount to NAV, creating substantial value for shareholders.

MAIN Stock Vs. CION Stock: Balance Sheets

MAIN’s investment grade credit rating is evidenced by its fairly low leverage ratio of 43.31%. Moreover, it has plenty of liquidity with $420 million, signifying a solid financial position against an enterprise value of $5.2 billion. Its capital structure is well-balanced with a combination of secured, floating-rate revolving debt, and unsecured, fixed-rate long-term debt.

CION, meanwhile, has a higher – though still reasonable – leverage ratio of 1.03x, while it also has plenty of liquidity and a fairly well-laddered debt maturity ladder, especially after recently refinancing a substantial amount of its debt.

Overall, we give MAIN the edge here given its investment-grade credit rating and lower leverage ratio.

MAIN Stock Vs. CION Stock: Business Models

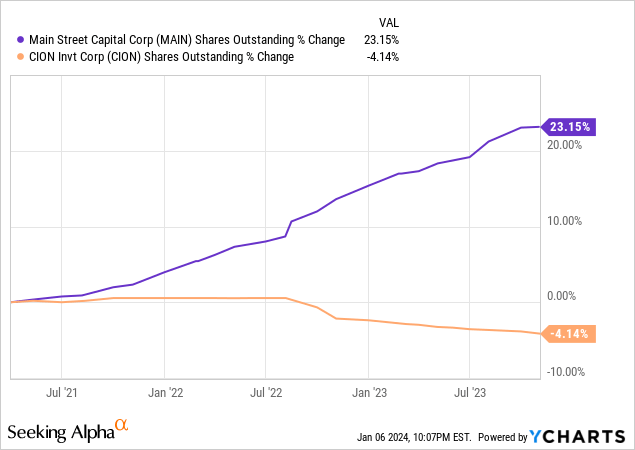

MAIN’s investment strategy is diversified across its Lower Middle Market, Private Loan, and Middle Market segments. They focus primarily on secured debt investments and complement those investments with equity growth investments. This approach has served MAIN very well over the long term, enabling them to generate attractive returns for shareholders and – as a result – trade at a significant premium to NAV. MAIN prudently takes advantage of this by regularly issuing new stock, thereby growing its NAV per share which – in turn – enables it to grow its dividend consistently as well. This fuels a virtuous cycle that has delivered phenomenal long-term outperformance for shareholders.

CION’s investment portfolio, meanwhile, is diversified across 109 companies in 24 industries and is primarily focused (87.8% of its investment portfolio) on senior secured loans, including 85.7% in first-lien investments. With its non-accruals sitting at just 1% on a fair value basis, CION’s investment portfolio appears to be operating at a very high level right now. MAIN’s non-accruals also sit at ~1% on a fair value basis, indicating that its underwriting performance is equally strong, if not stronger, given that only 68.8% of its portfolio is invested in senior secured debt.

CION’s capital allocation strategy is a bit different from MAIN’s given that its stock trades at a steep discount to NAV rather than a steep premium. As a result, instead of issuing shares to drive NAV per share accretion, CION is repurchasing shares at a steep discount, driving NAV per share accretion in the process.

It is also important to note that – while MAIN has a nine-year dividend growth streak – CION has been more conservative with growing its own quarterly dividend, though both have been paying out special dividends to maintain compliance with BDC regulations that they must pay out 90%+ of taxable income in the wake of rising net investment income due to rising interest rates.

A final consideration to keep in mind is that MAIN is internally managed whereas CION is externally managed. As a result, MAIN’s expense ratio is much lower than CION’s (2.63% vs. 7.35% on a non-leveraged basis, according to cefdata.com).

Overall, we think that MAIN’s business model is superior to CION’s across a full business cycle. However, given that we believe that now is a prudent time to be more defensive and value-oriented, rather than aggressive and growth-oriented, we think that CION’s business model – with its greater focus on senior-secured debt investments compared to MAIN and its emphasis on buying back stock instead of issuing stock – is in a more favorable position, MAIN’s lower expense ratio notwithstanding.

MAIN Stock Vs. CION Stock: Dividend Analysis

Both companies currently enjoy strong dividend coverage ratios. MAIN has had such strong dividend coverage that it has paid special dividends for nine quarters in a row while also growing its regular monthly dividend at a healthy clip (growing it five times out of the past six quarters). In fact, in the third quarter, MAIN’s distributable net investment income exceeded its regular monthly dividends by a whopping 51%. Moving forward, analysts expect its dividend to continue growing at a

Clearly, MAIN’s base dividend is very safe and it appears highly likely that it will continue to deliver attractive supplemental dividends to shareholders for the foreseeable future. Moreover, analysts currently forecast its dividend to grow at a 9.2% CAGR through 2025, making it an exceptional dividend growth stock.

CION, meanwhile, also enjoys strong dividend coverage, with its net investment income exceeding its regular quarterly dividend by an even more impressive 62% during the third quarter. This gave management plenty of flexibility to invest in new loans, pay out substantial special dividends, and buy back shares. Management also mentioned on its latest earnings call that they may increase the pace of their share buyback program in the coming quarters.

That being said, despite their exceptionally strong dividend coverage ratio, management said it plans to keep its regular quarterly dividend steady “for now.” While it is uncertain why this is the case exactly, it appears that management wants to maintain maximum financial flexibility moving forward as it continues to strive to diversify and grow its investment portfolio and buy back stock in an attempt to close its steep gap to NAV per share. Still, some growth in the regular quarterly dividend and/or a major acceleration of the buyback would go a long way toward signaling management’s confidence in the stock and likely lead to a significant upside in the stock price.

MAIN Stock Vs. CION Stock: Valuations

When it comes to valuation, CION is the clear winner. MAIN trades at a whopping 1.54x premium to its NAV – which is roughly in-line with its five-year average of 1.58x – and also trades at a lower NTM dividend yield (6.56%) than its five-year average (7.09%). That being said, its P/E ratio of 11.10x is meaningfully lower than its five-year average of 14.37x, but this is likely only temporary due to the elevated state of short-term interest rates.

CION, meanwhile, trades at a steep discount to its NAV (0.71x), offers a very attractive dividend yield that is nearly double MAIN’s (12.63%), and also trades at a very cheap P/E ratio of just 6.76x. Both its dividend yield and its P/E ratio are at clear discounts to its historical averages, while its P/NAV discount is roughly in line with its historical average. With CION, you are getting more than twice the book value for every dollar spent than you are with MAIN and nearly twice as much dividend income.

MAIN Stock Vs. CION Stock: Risk Assessment

Both MAIN and CION are positioned to thrive in an environment where the economy avoids any sort of meaningful downturn and interest rates remain somewhat elevated. As a result, if the U.S. economy can navigate a soft landing, the Federal Reserve may be able to only slowly cut interest rates while non-accruals and defaults on MAIN’s and CION’s investments will likely not spike much at all either.

However, if the economy does go into recession and the Fed is forced to slash interest rates aggressively, this could be a very bad scenario for MAIN and CION, as the recession will likely lead to a sharp uptick in non-accruals and potentially even defaults in their respective investment portfolios while their net investment income will also likely suffer a blow given that they both have significant exposure to floating rate loans, which will see their rates drop.

Another risk to keep in mind that is unique to CION is the fact that it has an unusually high percentage of its loans invested in PIK (payment-in-kind) loans. While the company explains in its annual report that it structures many of its loans this way on purpose to earn higher returns and to better support unique circumstances and structures for its borrowers, these loans are inherently riskier. As a result, CION could see a higher uptick in non-accruals than many of its peers during an economic downturn. That being said, the senior secured structuring of the vast majority of its loans and the deep discount to NAV more than compensate for this risk factor.

MAIN Stock Vs. CION Stock: Investor Takeaway

MAIN is clearly a phenomenal BDC, and there is a strong case to be made that it is the best publicly traded BDC there is. However, price is what you pay and value is what you get. Therefore, while MAIN is certainly valuable and definitely deserves to trade at a premium to NAV, given the current macroeconomic environment where short-term interest rates are likely to fall in the near future and we face a real risk of falling into recession, we do not think that it deserves to trade at nearly the premium it currently enjoys.

Meanwhile, CION only has a short track record as a publicly traded BDC and does not have nearly the prestige, low expense ratio, or dividend growth outlook that MAIN enjoys. However, its underwriting performance has been strong, its balance sheet is in fine shape, its investment portfolio is conservatively positioned, and its valuation is extremely cheap. While CION may deserve to trade at a discount to NAV given its higher expense ratio and less-proven track record, we think its current discount is far too steep and its dividend yield – which appears quite safe at the moment – looks extremely attractive.

As a result, we rate MAIN a Hold and CION a Strong Buy.

Read the full article here

Q3 2024 Earnings Call Transcript")

")

")