")

")

Very early this year, I found myself being quite bearish when it came to the homebuilding market. Although I understood that there was a national housing shortage, high interest rates and elevated prices that interest rates were raised in order to combat, were already having a major impact on the near-term demand for houses. My expectation at that time was that, for at least this year and possibly a good portion of next year, we would see significant weakness in the space before ultimately enjoying a massive rebound in demand. Interestingly, my timeline ended up being off rather considerably. While we did see additional weakness heading into the middle of the year, it was also around that time that we began to see signs of a recovery in demand.

The data pointing to a recovery ultimately led me to reaffirm my bullishness in some names that I had written about earlier in the year. But one company that I found myself bullish on even as weaknesses continued to grow was Meritage Homes Corporation (NYSE:MTH). Because of how cheap the shares were and because of my long-term outlook for the space, I ended up keeping the company rated a “buy.” That was back in late July of this year.

Fast forward to today, and shares have fallen by 5% compared to the 3.4% drop seen by the S&P 500 (SP500). But when you look at the newest data provided by management, it becomes clear that the market is misjudging the company rather considerably. Moving forward, I expect additional good things from the enterprise. So even though the market has so far disagreed with my assessment, I am keeping the company a solid “buy” at this time.

The picture is getting better… mostly

Author – SEC EDGAR Data

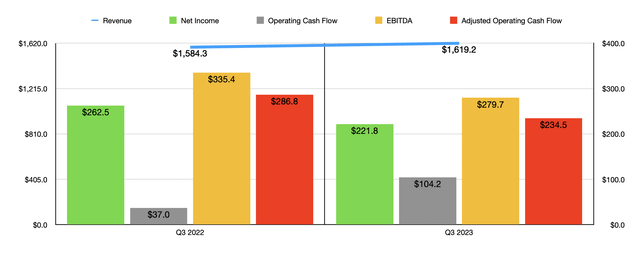

To understand why I continue to be bullish about Meritage Homes, we need only look at data covering the third quarter of the company’s 2023 fiscal year. During that quarter, revenue for the business came in at $1.62 billion. That represents an increase of 2.2% compared to the $1.58 billion generated one year earlier. Even though the average sales price of a home closing for the company fell from $450,000 to $443,000, the company benefited from an increase in the number of closings from 3,487 units to 3,638 units.

Author – SEC EDGAR Data

On the bottom line, the picture was a bit more complicated. Most of the profitability metrics for the company actually worsened during this time. Net income, for instance, declined from $262.5 million in the third quarter of 2022 to $221.8 million at the same time this year. Management attributed this decline to a couple of factors. For starters, in order to incentivize additional customers, the company began offering higher buyer financing incentives. It also had to deal with higher land development costs.

Most other profitability metrics followed suit. The one exception was operating cash flow, which skyrocketed from $37 million to $104.2 million. But if we adjust for changes in working capital, we would get a decline from $286.8 million to $234.5 million. Meanwhile, EBITDA for the company dropped from $335.4 million to $279.7 million.

Author – SEC EDGAR Data

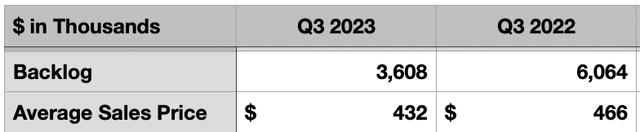

All of this looks fine at first glance. But one of the really interesting things about the home building market is that the companies in it invariably report data that could be used as a leading indicator. The fact of the matter is that homes take a while to build and that means there is a lag between when problems develop in the space and when those problems start showing up in the form of revenue and profits. Significant declines in backlog and new orders were ultimately what drove me to become bearish in the space earlier this year.

Even today, the backlog for Meritage Homes is down considerably compared to where it was last year. As of the third quarter, it came in at 3,608 units, which represents a sizable decline from the 6,064 units in backlog at the same time last year. And the average price of a home in backlog has fallen from $466,000 to $432,000.

Author – SEC EDGAR Data Author – SEC EDGAR Data

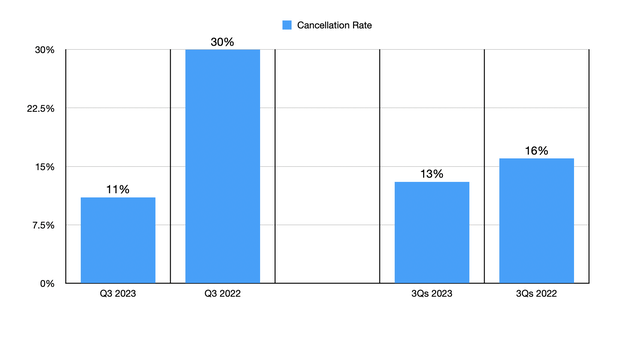

Somebody might look at this data and be scared about what the future holds. But I am here to tell you that there has been a considerable improvement for the company. And this is in the form of orders. Net new orders for the company in the third quarter alone came in at 3,474 units. That represents an increase of 50.4% over the 2,310 units ordered at the same time last year. Add on top of this the fact that the average sales price has grown from $422,000 to $430,000, and it is clear that new buyers are coming into the picture. Add on top of this the fact that the cancellation rate that the company has seen has plummeted from 30% in the third quarter of last year to only 11% at the same time this year, and investors should be very happy.

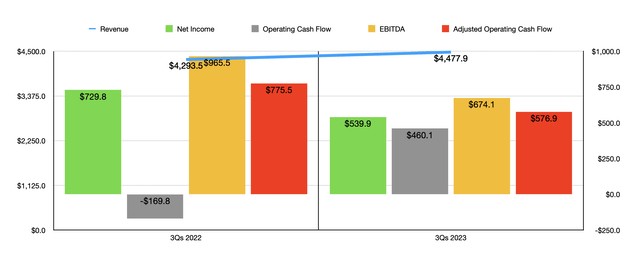

As you can see in the table above, as well as in the chart below, I also include the data for the first nine months of this year relative to the same time last year. The overall picture is very similar. But it is obvious that the data from the third quarter is particularly bullish compared to the year as a whole. This can be seen by looking at both the new order rate and the cancellation rate changes, the latter of which is in the second graphic above.

Author – SEC EDGAR Data

When it comes to the final quarter of this year, management is forecasting earnings per share of between $4.84 and $5.43. If we use the midpoint of guidance, that should translate to $190.4 million of profit. That implies $730.3 million in profit for the year as a whole. No guidance was offered when it came to other profitability metrics. But approximations that I did indicate that adjusted operating cash flow should be around $781 million while EBITDA should come in somewhere around $779.9 million.

Author – SEC EDGAR Data

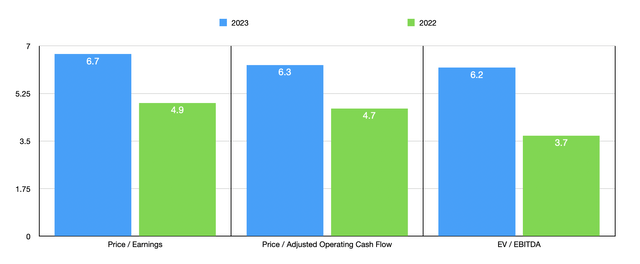

Using these figures, I was able to value the company as shown in the chart above. That chart also has valuations using data from 2022. As you can see, the company is more expensive on a forward basis. But with multiples in the mid-single digit range, the stock is still very attractive. I then compared the firm to five similar companies in the table below. On both a price-to-earnings basis and an EV-to-EBITDA basis, only one of the five firms was cheaper than our prospect. And when it comes to the price to operating cash flow approach, four of the five ended up being cheaper.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Meritage Homes | 6.7 | 6.3 | 6.2 |

| Beazer Homes USA, Inc. (BZH) | 4.6 | 2.6 | 6.7 |

| Century Communities, Inc. (CCS) | 9.0 | 5.3 | 8.9 |

| Legacy Housing Corporation (LEGH) | 7.1 | 44.3 | 5.4 |

| Dream Finders Homes, Inc. (DFH) | 8.7 | 6.0 | 6.4 |

| Landsea Homes Corporation (LSEA) | 8.3 | 3.4 | 12.7 |

Takeaway

Although it may seem like a peculiar time to be bullish on the homebuilding market, the data speaks for itself. I have seen this kind of change in other firms in the industry, so it is clear that it is industry-wide. There’s also the fact that interest rates are either at the highest point they will be or awfully close. This suggests to me that, once interest rates drop, the picture will become much more attractive very rapidly. But even if it doesn’t, the data supports a bullish outlook. So because of that, I’ve decided to keep Meritage Homes Corporation rated a “buy” for now.

Read the full article here

")

")

Q3 2024 Earnings Call Transcript")

")