")

The Chinese electric vehicle (“EV”) space continues to struggle to rebound from covid restrictions and the lack of subsidies that caused a rush to purchase vehicles at the end of 2022. NIO Inc. (NYSE:NIO) has fallen flat to start 2023, with sales growth not matching internal targets, though the EV company is making progress. My investment thesis remains ultra-Bullish on the breakout potential in the sector, though NIO continues to struggle to grow beyond prior sales peaks.

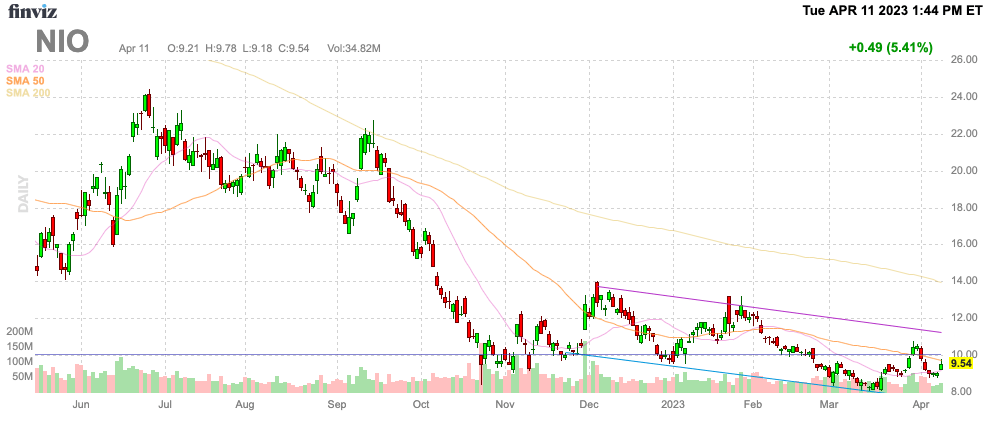

Source: Finviz

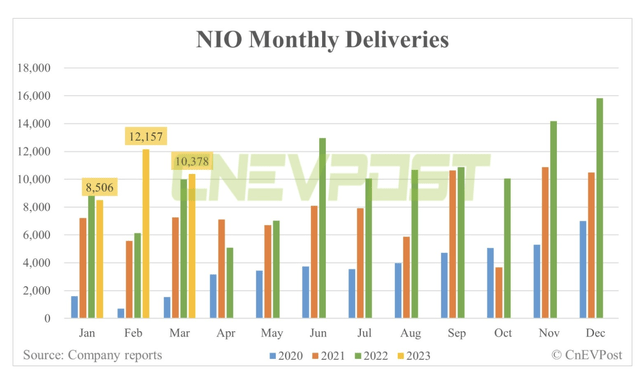

March Struggle

After NIO reported strong deliveries in February, the Chinese EV company was back to reporting weak numbers in March. The company reported 10,378 vehicle deliveries during March, down from the 12,157 deliveries in February.

Source: CnEVPost

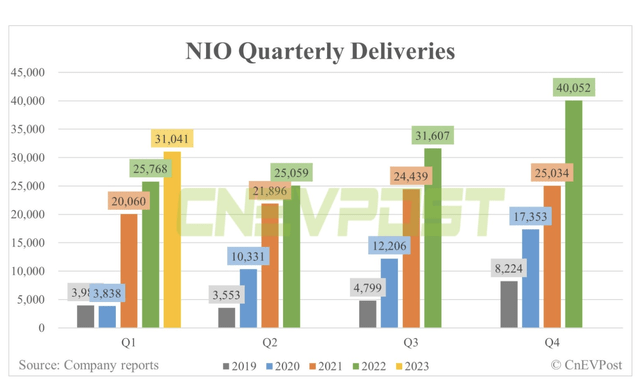

In total, NIO delivered 31,041 vehicles in Q1’23. The amount was up from last Q1, but the Chinese EV company is still struggling to consistently deliver vehicles in excess of 10K monthly after originally topping this delivery level back in September 2021.

NIO continues to have wildly volatile monthly delivery numbers, but the quarterly amounts show a much more consistent growth pattern. The Q1 2023 numbers were the highest Q1 numbers in corporate history, topping the 25,768 vehicles delivered back in 2022.

Source: CnEVPost

As the above chart shows, quarterly sales tend to trend higher throughout the year with the highest vehicle deliveries in the last quarter of the year. NIO could definitely be on a record delivery schedule, if the momentum from Q1 continues in the current quarter, but the last couple of years have seen sequentially flat numbers before a 2H sales bump.

NIO continues to aggressively roll out the battery charging plans, including 1,339 battery swap stations and 1,285 charging stations now. Of course, for these numbers to matter, the company has to show more consistent growth in actual EV sales.

Breakout Potential

When reporting Q4 2022 results, the CEO forecast the company doubling EV sales this year to 250,000 vehicles. CEO William Li made the following statement on the earnings call:

In a nutshell, our target is still to double the volume in this year, and our teams are quite confident to achieve this target. When it comes to the profitability, this is closely bundled together with the gross margin. So if the raw material cost reduction can be of expectations, like I explained before then for the fourth quarter, we believe this probably can still achieve the target that we said before.

As Q1’23 deliveries only grew around 20% over Q1’22 levels, the CFO went on Bloomberg Television and confirmed the goal of hitting these aggressive targets with the following statement:

We are very confident to achieve our sales target in 2023. The company hopes to achieve the target with new models, expanding its charging and battery-swapping network, and unlocking autonomous driving technologies.

In our opinion, the company isn’t doing shareholders any favor setting up the market with goals that are too aggressive. Analysts forecast sales growing 74% to $12.5 billion, and the CEO latter suggested some investments would reduce the ability to report full profitability for the year.

Either number would be impressive, but the market won’t necessarily be happy with NIO hitting a target far below the levels set by the executives. After all, NIO has to hit the following quarterly vehicle delivery targets to just double sales this year:

- Q2’23 – 50.1K

- Q3’23 – 63.2K

- Q4’23 – 80.1K.

Remember, NIO has to produce these quarterly vehicle delivery targets to double the 2022 levels. The Chinese EV company still has to produce an additional 20,495 vehicles to double the Q1 production levels after not coming anywhere close to doubling sales in the March quarter.

Ultimately, the market will reward massive progress towards growth by starting to produce over 15K to 20K in monthly deliveries, leading to a quarterly delivery level topping 50K. NIO won’t need perfection to generate upside to the stock from levels around just $9.

Where the stock becomes incredibly appealing is when profits arrive and NIO still has a large cash balance. The market cap is only $15 billion now, and a large cash balance exceeding $6 billion would suddenly become a major asset not included in prior analysis with the way the Chinese EV company was burning cash.

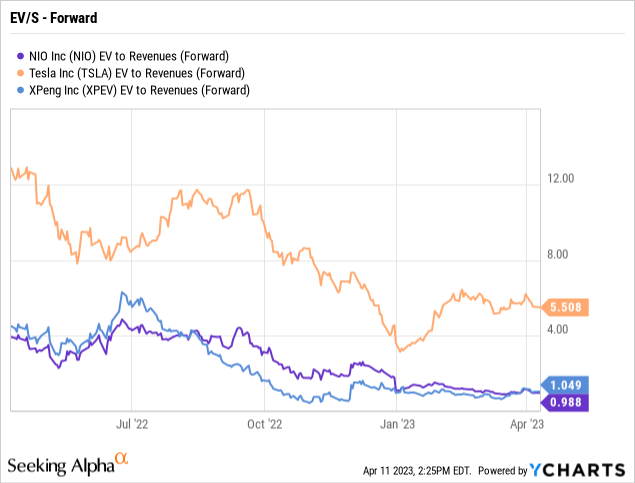

Our base case isn’t for NIO to ever obtain the rich valuation premium of Tesla, Inc. (TSLA), but a Chinese company with faster growth would warrant more consideration going forward. Remember, the stock only trades at a forward EV/S target for 2023 of 1x, but the number is similar to XPeng (XPEV).

The market isn’t convinced NIO can produce the stated growth targets despite the promising technology surrounding the EVs around battery swap and self-driving technology.

At NIO Day 2022 held on December 24, 2022, the company launched the EC7 as well as the new ES8. These vehicles have deliveries to begin in May and June 2023, respectively. A big question market is what happens to demand in April and May heading into these launches and whether NIO can sustain increasing sales without having to constantly launch new models to fend off competition.

Takeaway

The key investor takeaway is that NIO Inc. continues to make slow progress while the stock has significant upside potential from hitting aggressive targets. The company forecasts being breakeven by year-end for the NIO brand. Under these scenarios, the stock has the upside potential for major multiple expansion considering where Tesla trades with a forecast for 25% growth, while NIO Inc. could exceed those growth rates by several multiples.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")

(NASDAQ:MU)")

")

JPMorgan Annual Healthcare Conference – (Transcript)")

")

")