(SP500)")

The S&P 500 (SPY) briefly exceeded 5500 this week and the 5400 inflection point pointed out in last weekend’s article was never in danger of breaking. In theory, it should be quite simple to buy against these levels – the risk is defined (and low), plus the trend is clearly higher so odds are in your favor. In practice, it is, for one reason or another, very difficult; there are always things to worry about.

One of these days, buying against an inflection point will not work. We can then take a small loss and re-assess. Until that day, it is the one of the best approaches to joining the trend, even when we think it might be in the final stages. No-one really knows where it could end up.

This week’s article will update inflection points and outline expectations for the last week of Q2. Various techniques will be applied to multiple timeframes in a top-down process which also considers the major market drivers. The aim is to provide an actionable guide with directional bias, important levels, and expectations for future price action.

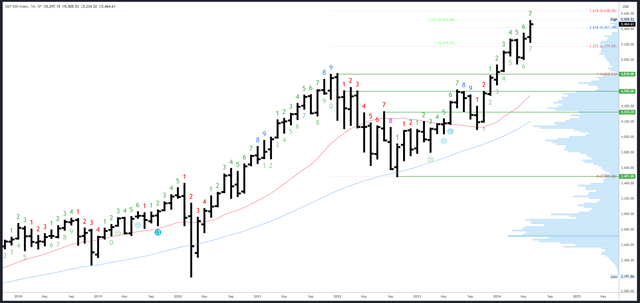

S&P 500 Monthly

The June bar and the Q2 bar will close this Friday. This has been the third very strong quarter in a row, and as the last two closed near the highs, it likely does the same. As an aside, all three quarterly bars will have closed on a Friday, which must be fairly unusual and may have aided the strong closes. The Q3 bar will close on a Monday.

A strong close near 5500 would project continuation higher early in July.

With only 5 days left in June, the bar is set high for a bearish bar to form with a close back inside May’s range below 5341.

SPX Monthly (Tradingview)

With the S&P500 trading into new all-time highs, Fibonacci extensions and measured moves provide targets. 5522 is the next minor measured move (it is where the rally from the Oct ’23 low = 1.272% of the Oct ’22 – July ’23 rally). The next major level comes from the 1.618* expansion of the 2021-2022 bear market and is way up at 5638.

May’s high of 5341 is now important as the S&P500 has exceeded it significantly. Should prices drop back inside May’s range, the bias would shift bearish, especially if the June bar closes near its open of 5297.

June is bar 7 (of a possible 9) in an upside Demark exhaustion count. These counts can have an effect from bar 8 onwards so a reaction could be seen in July.

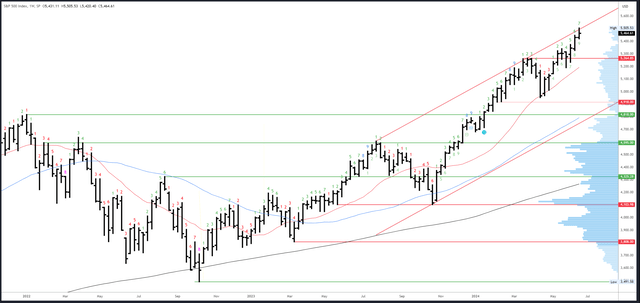

S&P 500 Weekly

The rally has reached and reacted from the top of a potential channel which may limit progress. This doesn’t necessarily mean the rally will reverse, though, and it could simply hug the channel as it moves higher.

This week’s bar made a higher low, higher low and higher close which is obviously bullish, but the close was off the highs and this shifts the bias more neutral for next week.

SPX Weekly (Tradingview)

The weekly channel high will be around 5510 next week.

This week’s low of 5420 is initial support. 5265 is a major level, but should not be tested if this rally is to stay strong.

Next week will be bar 8 (of 9) of an upside Demark exhaustion count. As noted earlier, these counts can have an effect from bar 8 onwards so a reaction is possible in the coming weeks. The monthly/weekly counts will be in sync from the first week in July.

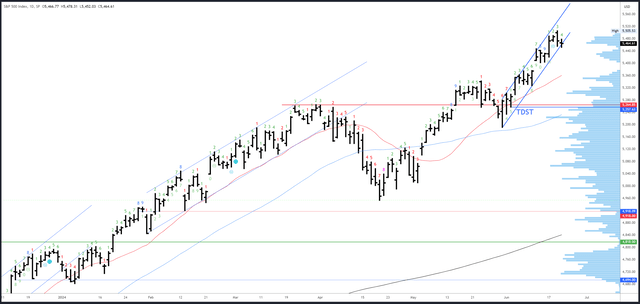

S&P 500 Daily

Thursday’s higher open and fade formed a classic exhaustion gap and was accompanied by a big reversal on Nvidia (NVDA). This looks very similar to the pattern formed on 8th March which marked an intermediate top in NVDA, but not for the S&P500 which consolidated and then made new highs several weeks later. Perhaps a similar scenario unfolds again.

This week’s reversal pattern likely leads to a break in the daily trend channel and some mild weakness at the start of next week. We can assume this is just an ordinary bullish consolidation / dip as long as 5400 holds, and this remains the major inflection.

SPX Daily (Tradingview)

Thursday’s 5505 high is the only real resistance.

On the downside, 5440 is initial support, but the big level is 5400.

An upside Demark will be on bar 5 on Monday. A reaction could be seen on Thursday or Friday (bars 8 or 9) but this relies on the count continuing. Monday has to close above 5473 for this to happen.

Drivers/Events

This week’s data was cool but mostly better than expected and not at all indicative of an economy in imminent danger. With the odds of cuts in September now around 65%, data like this is ideal for the S&P500 – not too hot to delay cuts and not too weak to fret over the economy.

Next week’s scheduled events are on the quiet side until Thursday when GDP, Unemployment Claims and Pending Home Sales are due for release. It is doubtful if these will move markets much, especially ahead of the highlight of the week, Friday’s PCE Index. This is the Fed’s preferred inflation gauge and a soft reading would likely boost the odds of a September cut.

Probable Moves Next Week(s)

In the short-term, Thursday’s reversal could lead to further downside to 5440, perhaps 5400, which remains a key inflection for this stage of the rally. A dip near these levels could be a place to “hold your nose and buy.” You might not like it, it might not work, but it is the right approach as Q2 likely closes strong and the higher timeframes continue to have a bullish bias.

Read the full article here

")

Q4 2024 Earnings Call Transcript")

")