")

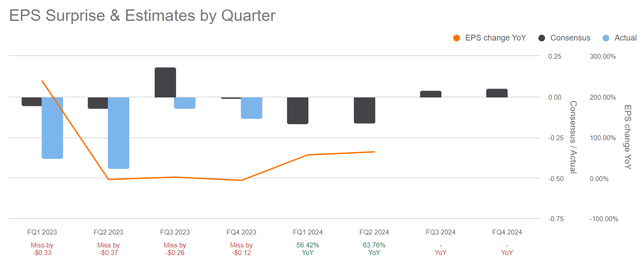

Warner Brothers Discovery (NASDAQ:WBD) released first quarter earnings last week. The media giant has been scrutinized for earnings performance and high leverage since its merger. Back in February, I took a bullish stand on Warner Brothers Discovery through the sale of cash secured puts. While the first quarter earnings report disappointed by missing both revenue and earnings estimates, I believe there are current and upcoming catalysts to stay bullish on WBD stock.

Warner Brothers Discovery Earnings Results

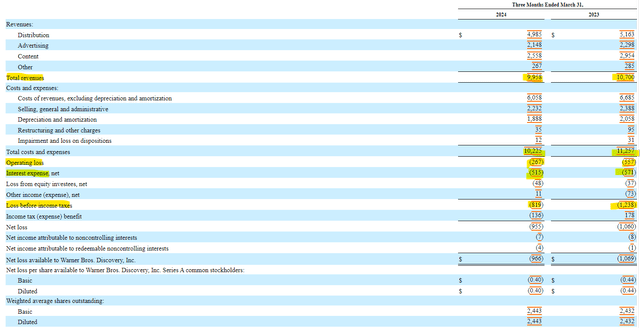

Warner Brothers Discovery saw a broad decline in revenue across all segments of its business in the first quarter. Fortunately, the $700 million drop in revenue was offset by a $1 billion drop in expenses as the company did a well containing variable costs. Despite the positive variance, there was still an operating loss of $267 million and a loss before taxes of $819 million.

SEC 10-Q

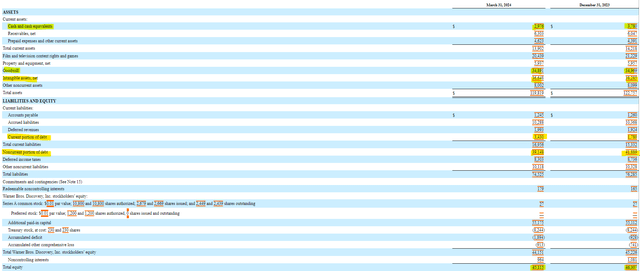

On the balance sheet, Warner Brothers Discovery paid down $1 billion of debt despite running an operating loss. Some of the debt paydown came from cash as the balance fell by $800 million. Shareholder equity declined by $1 billion, and while many investors may see the discount between market capitalization and shareholder equity as an opportunity, it is important to note that Warner Brothers Discovery’s balance sheet is loaded with intangible assets that must be amortized.

SEC 10-Q

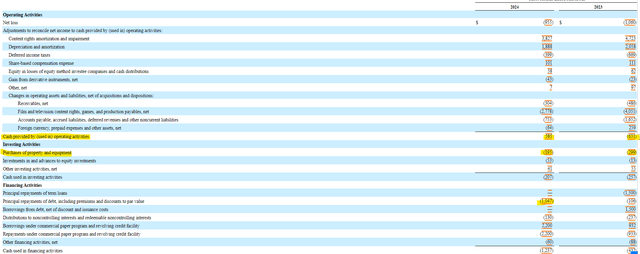

The bread and butter of Warner Brothers Discovery comes from its cash flow statement. Because so much of the business’s expense is tied to depreciation and amortization, the company generates healthy cash flows. In the first quarter, Warner Brothers Discover generated $585 million in operating cash flow and $390 million in free cash flow compared to a burn of $631 million and $930 million in the same quarter a year ago, respectively. The free cash flow plus $600 million in cash went into paying down debt by more than $1 billion in the first quarter.

SEC 10-Q

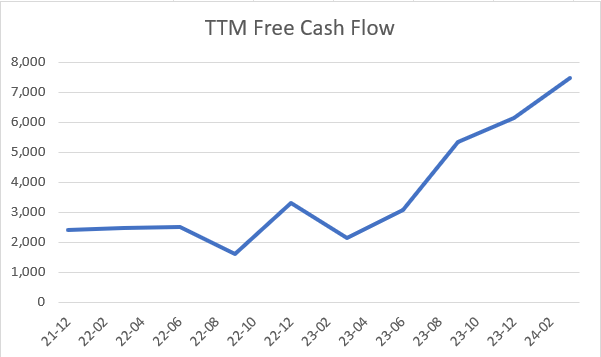

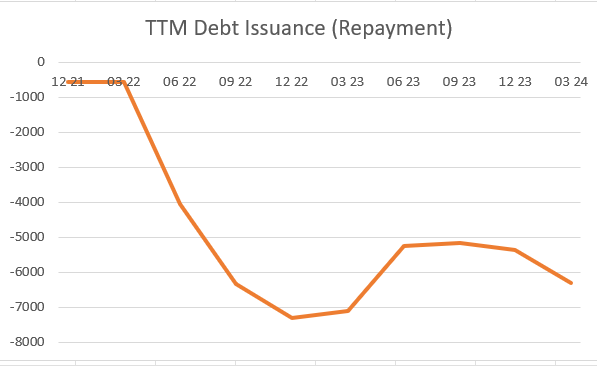

In addition to strong cash flow in the first quarter, Warner Brothers Discovery’s free cash flow on a trailing twelve-month basis surged to over $7 billion. More than $6 billion of that free cash flow has been used to pay down debt as the company commits itself to deleveraging. Continued debt reduction should lead to lower interest expenses and higher earnings in the future.

TIKR TIKR

WBD’s Commitment to Debt Reduction

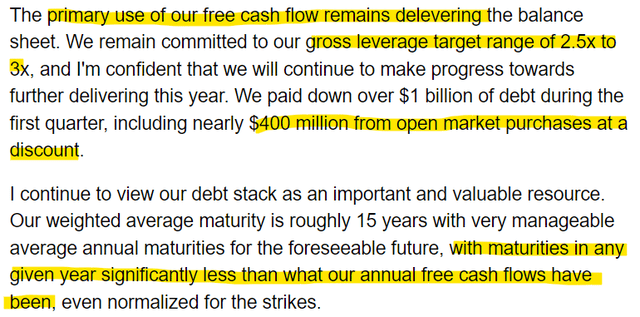

Warner Brothers Discovery’s high debt load has been scrutinized by many analysts. The company is not only using its free cash flow to pay down debt, but management has publicly committed to deleveraging further. Management mentioned in the earnings call that it was utilizing open market purchases at a discount as part of its debt reduction strategy to get to its 3x gross leverage target. On the same day as its earnings report, Warner Brothers Discovery announced a cash tender offer to purchase up to $1.75 billion of long-term notes with cash on hand.

Earnings Call Transcript SEC 10-Q

Can Warner Brothers Discovery Attain Profitability?

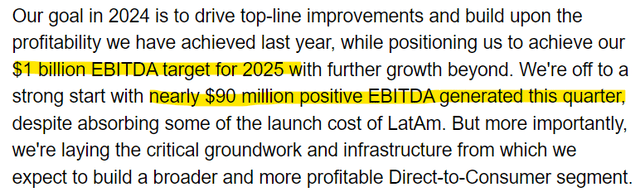

While free cash flow and debt reduction numbers are great, Warner Brothers Discovery will serve its investors well by generating profits. Despite an earnings loss below estimates during the first quarter, analysts believe that the company will begin generating small profits in the second half of the year with full year profitability attained in 2025. Management has also set a $1 billion EBITDA goal for 2025.

Seeking Alpha Seeking Alpha Earnings Transcript

What Trade is Best for Warner Brothers Discovery Bulls?

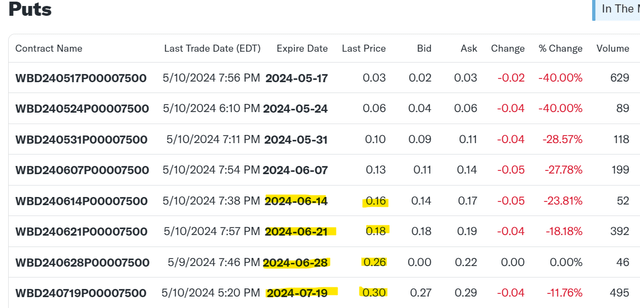

While purchasing shares outright may be the best play for some, I am still rolling over cash secured put options. My latest option contract expires this week, and I will be looking to initiate a new contract that expires between mid-June and mid-July. The income on these contracts is currently priced above 20% annualized returns and softens the cost of entry from $7.50 to between $7.20 and $7.34 per share. If assigned shares on a selloff, investors can generate additional income by selling covered call options.

Yahoo Finance

Conclusion

Warner Brothers Discovery continues its turnaround efforts. The media company is still struggling to attain profitability under the weight of high leverage following its merger. Despite these struggles, free cash flow is surging, and management has prioritized deleveraging. Analysts are confident that profitability will return in the next few quarters and therefore shareholders should start to see the share price rally accordingly.

Read the full article here

(COST)")

")

")

")

(NYSE:SNOW)")

")

Q4 2024 Earnings Call Transcript")